On 12 January 2023, the European Union’s Foreign Subsidies Regulation (“FSR”) entered into force, and it has already started to apply on 12 July 2023. The impact of the FSR will be significant, in particular for M&A transactions, given that it will result in a substantial burden for businesses. In this article we provide an overview of the basic concepts of the FSR and its implications and suggest ways companies can prepare in order to comply with the relevant regulatory burdens.

- What’s new?

This new set of rules enables the European Commission (“EC”) to examine foreign subsidies granted by non-EU countries that distort the EU internal market.

The FSR introduces an additional review regime, separate from the existing merger and foreign direct investment (FDI) control regimes, by requiring prior notification to and approval from the EC of transactions involving companies that have received financial support from non-EU countries. It also enables the EC to investigate any commercial activity in the EU (deal-related or not) where foreign subsidies may have a distortive effect in the EU internal market.

Although the filing requirements will enter into force on 12 October 2023, the EC is already entitled to conduct ex officio investigations from 12 July 2023. In fact, already in August 2023 the EC received the first FSR complaint regarding an alleged Qatari investment received by Paris Saint-Germain FC.

- When is a notification required?

The FSR targets all companies, private or public, that are established in the EU (via a subsidiary or permanent establishment in an EU member state), generate turnover in the EU and have received any form of direct or indirect financial contribution from a non-EU country or public body (or private body acting on behalf of a public body) (“foreign financial contributions”).

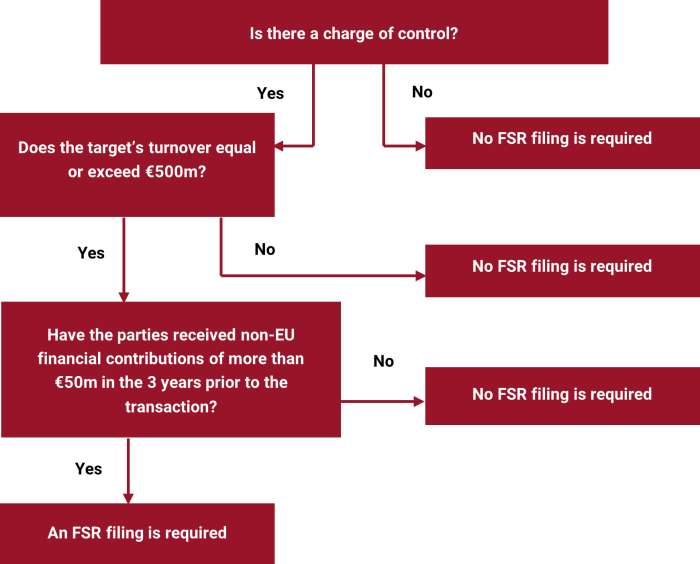

A filing is required in cases where:

- the target (in case of an acquisition), one of the merging parties (in case of a merger) or a joint venture generates an aggregate turnover in the Union of at least EUR 500 million, and

- all parties combined were granted financial contributions of more than EUR 50 million from third countries in the three years preceding the concentration.

Filings have a suspensory effect, meaning that a transaction shall not be completed prior to FSR clearance.

- What stands for a foreign financial contribution?

Foreign financial contributions are defined broadly and may include:

- the transfer of state funds or liabilities: such as grants, interest-free or low-interest loans, capital injections, fiscal incentives, guarantees, debt forgiveness, debt to equity swaps or rescheduling, contributions in kind or state-funded R&D;

- the foregoing of state revenue: such as tax exemptions or reductions, tax incentives or the granting of special/exclusive rights without adequate remuneration in line with normal market conditions.

The financial contribution needs to be selective, i.e., to confer a benefit on one or more specific companies or industries.

- When will the filing obligation begin?

If the thresholds are met, the filing obligation will start to apply as of 12 October 2023. The filing requirements also apply for deals that are signed on or after 12 July 2023, but which have not closed before 12 October 2023.

- What information is included in the notification?

Detailed information is only required for foreign financial contributions which may qualify as ‘most likely distortive subsidies’, provided that the individual amounts of those financial contributions are equal to or above EUR 1 million[1]. Such information includes, inter alia, the following:

- the form of the financial contribution;

- information on the granting authority or entity;

- the amount, purpose, economic rationale, main elements, and characteristics of the financial contribution;

- conditions attached to the financial contribution; and

- whether the financial contribution confers any selective advantage to the recipient.

For all other financial contributions, details per financial contribution are not required. Rather, it is sufficient to fill in an overview table with a total estimate of financial contributions obtained in the three years prior to the notified transaction per type and per third country. Supporting documentation is only required for the first category of financial contributions.

There are also some types of financial contributions that do not need to be included in the notification at all, although these need to be taken into account when assessing the notification thresholds.

The parties are also able to request waivers from the EC for information that is not reasonably available and not necessary for the examination of the case.

- How does the filing obligation affect the timetable of a deal?

The FSR review process is similar to the merger review before the EC, including a Phase 1 review of 25 working days, and a Phase 2 review of up to 90 working days (or up to 105 working days where the parties offer commitments), in case of substantive concerns[2]. Commitments can only be offered during Phase 2.

- Is there a substantive test for the EC’s review?

The EC assesses whether a foreign subsidy distorts the EU internal market. In case a foreign subsidy is deemed to be distortive, the EC may impose redressive measures, including, inter alia, repayment of subsidies, behavioural commitments or in exceptional cases block deals or even dissolve concentrations already concluded.

- What applies to private equity funds?

The EC has limited disclosure requirements only to the acquiring fund (or funds). In addition, private equity funds will not have to declare non-distortive financial contributions received by other funds managed by the same general partner, if their respective investor pools are different, provided that the following conditions are met:

- the fund which controls the acquiring entity is subject to the EU Directive on Alternative Investment Fund Managers[3] or equivalent legislation, and

- there are no or only limited economic or commercial transactions between the fund that controls the acquiring entity and other investment funds managed by the same investment company, including sales of assets, ownership in companies, loans, credit lines or guarantees.

However, investment firms are still required to track and assemble data on most financial contributions from their investors into funds, as well as any contributions or tax breaks received by their portfolio companies.

- How can companies prepare?

Given that the notification requirement will start to apply soon, companies shall consider the following:

- Conduct preliminary assessments on whether a FSR notification will be required for upcoming deals and if so, begin pre-notification discussions with the EC;

- implement an internal system to identify and monitor foreign financial contributions;

- coordinate legal strategy if multiple notifications are required (e.g., FSR, merger control, FDI review);

- consider additional contractual provisions in the deal documents (e.g., conditions precedent, effort obligations and cooperation clauses, long stop date, and representations and warranties);

- require relevant information during due diligence.

[1] These most likely distortive subsidies are listed in Article 5(1) FSR.

[2] The abovementioned timeframe within which the EC shall issue a decision may be extended up to 20 working days subject to the parties’ consent.

[3] Directive 2011/61/EU of the European Parliament and of the Council of 8 June 2011 on Alternative Investment Fund Managers and amending Directives 2003/41/EC and 2009/65/EC and Regulations (EC) No 1060/2009 and (EU) No 1095/2010 (OJ L 174, 1.7.2011, p. 1).